Turning 26: A Step-By-Step Guide to Your First Health Insurance Policy

Not long ago turning 26 wasn’t that big of a deal. You’re 10 years past your sweet 16, 8 years past becoming an adult, and 5 years past being able to buy alcohol. But in 2010 the Affordable Care Act (ACA) was signed into law and that created a new milestone for young Americans…turning 26.

Turning 26 now means you can no longer be on your parent’s health insurance policy. I know…it’s not nearly as big of a deal as driving, voting, or drinking but it does bring you one step closer to being a completely independent adult.

So let’s take a look at the 7 steps to finding your new health insurance plan. We’ll learn about what it means to have your own health insurance policy and which type of plan you should consider purchasing.

Turning 26 Step 1 – Do your homework (maybe)

Your assignment is to get a copy of your parent’s health insurance plan so you know what coverage you currently have. That way we have something to compare the new plans to.

You’ve spent probably at least 17 years of your life doing homework so getting more at this stage is the last thing you want right now. I understand. So I’ll make you a deal. Just like all the homework you’ve ever been assigned in the past, you probably don’t have to do this one.

Homework only serves a purpose if it helps you understand something you don’t get yet or helps you prepare for a test. Otherwise, it’s just another obstacle keeping you from the things you enjoy. The purpose of my homework assignment is no different. It’s to make sure you understand your current coverage under your parent’s policy.

Most of you are healthy and haven’t really used your parent’s health coverage much. If that’s you then skip the homework. If you are using the coverage then you will want to do the homework. Deal?

Turning 26 Step 2 – Take advantage of subsidies & get quotes

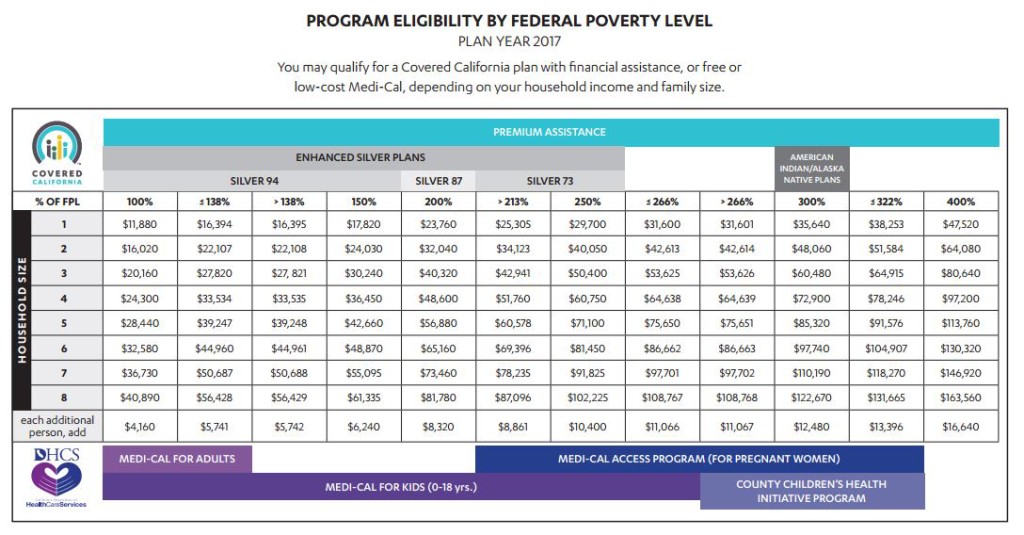

One good thing about the ACA is that there’s money available to help pay for health insurance for those who qualify. That financial help is called a subsidy. It’s kind of like financial aid for college. So it only make sense to start by seeing if your income is within the subsidy limits. Take a look at this chart below. Find your income and household size (hint: it’s just 1 unless you’re married or have children). If your household size is just 1, you’ll notice that this chart says you are likely eligible for a subsidy as long as your annual income is under $47,520. But keep in mind that subsidies are based on your income and also the cost of your policy. And since health insurance for a 26 year old is much less expensive than for most adults, subsidies actually start for incomes below around $32,000.

On the other end of the chart you’ll notice lower incomes are eligible for Medi-Cal. If your annual income is below $16,394, you’ll be enrolled in Medi-Cal which comes with zero premium (in other words, free!)

So if your income is below $32,000 and you do qualify for a subsidy, you’ll be using Covered California to enroll but you don’t have to do it alone. In fact, you shouldn’t do it alone. Use a Certified Insurance Agent, like those at Castaline Insurance Agency. You also may have heard of “Navigators” or “Enrollment Counselors”. You’ll want to stay away from those as they aren’t licensed and can’t give you advice on which plan to choose. Instead get the help of an agent such as Castaline Insurance Agency. We can show you how to assign an agent to your account at no cost. Take advantage of that.

Get quotes

If you don’t qualify for a subsidy, there is no need to use Covered California at all. In fact, there are many reasons you shouldn’t use it. So get an online quote somewhere else, like with us.

It’s easy. All you’ll need is your zip code and date of birth. You’ll be using an Agent here too. Once again, they’ll be your best source of unbiased advice because they work for you and can not only help you choose the right level plan, but also choose the right insurance company.

Turning 26 Step 3 – Check the doctor networks

Have your agent check the doctor networks. Seriously, take the time to do that. Insurance companies are using “narrow networks” to try and keep health insurance costs down. Narrow networks mean that you will have a smaller selection of doctors to choose from. They are the biggest downside to buying individual health insurance today. Is your doctor in the network for the insurance plan you’re thinking about buying? If not, you’ll likely want to find another company or get used to the fact that you won’t be seeing your doctor any longer.

Another problem arises when you have multiple doctors. One may be in the network while others are not. What do you do then? The answer, unfortunately, is compromise. You’ll have to go with the company that has your most important doctors and then find new ones to replace the others.

If you can’t find a plan that has your doctor, you still may be able to see her if you choose a PPO. PPOs cover out of network expenses, usually at 50% while HMOs and EPOs do not cover out of network expenses at all.

Turning 26 Step 4 – Choose a plan

Now that you know which insurance company has the doctors you need, it’s time to choose a plan that meets your budget and risk tolerance.

Catastrophic Plans

Because you’re under 30 years old, you qualify for a catastrophic plan if you choose. Catastrophic health plans have low premiums, high deductibles, and high cost sharing. They won’t cover normal out-of-pocket costs. In fact the only things a catastrophic plan will do for you is help you avoid a tax penalty, help you avoid bankruptcy, and limit the amount doctors can charge you versus a cash patient. Catastrophic plans aren’t even eligible for subsidy assistance.

So why get one? I don’t recommend catastrophic plans unless you are prepared to go without health insurance. In that case, you’re better off with something rather than nothing. Choose a catastrophic plan only if it is the only plan you can afford.

Bronze, Silver, Gold, Platinum

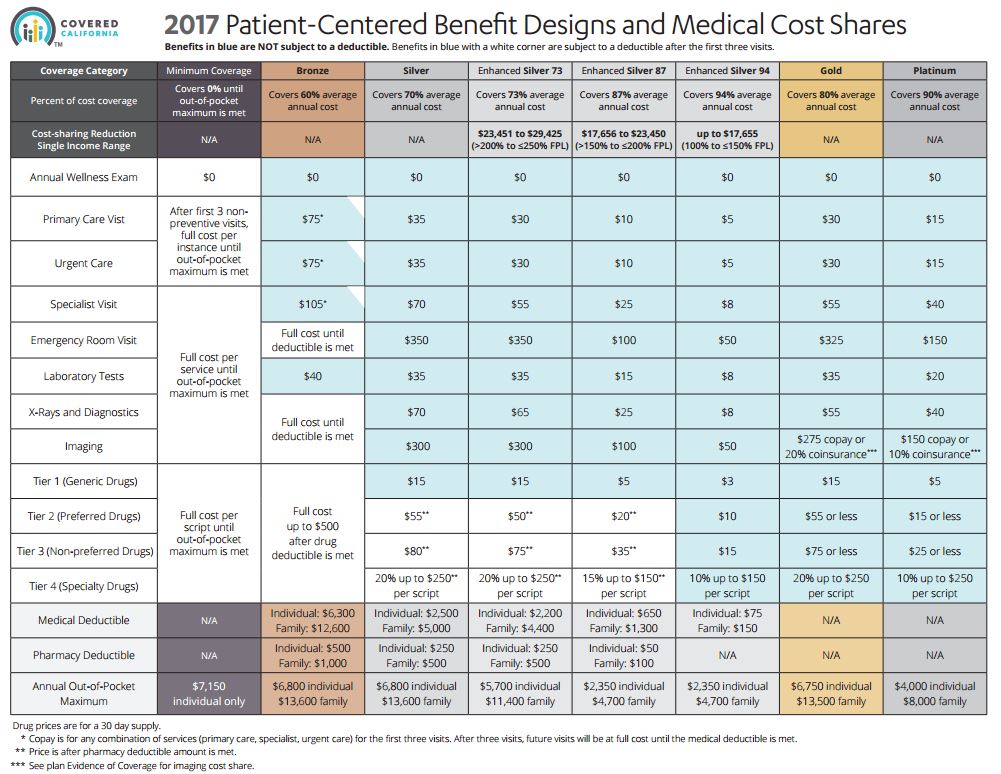

The remaining 4 options are named after metals. They range from Bronze (least coverage and least expensive) to Platinum (most coverage and most expensive). This chart on the following page from Covered California best illustrates the major coverage options.

Pay attention to the deductible (the portion you’ll pay before the insurance company begins paying), copays (the amount you’ll pay for each service you use), and the out of pocket maximum (the most you’ll be responsible for paying in a calendar year).

Choose the plan you can afford which offers the best coverage for your individual or family’s specific circumstance.

Turning 26 Step 5 – Apply online

Whether you’re using Covered California or buying an individual plan from an independent agent like Castaline Insurance Agency, complete an online application. This will speed up the process and will help you to avoid any errors that often seem to arise when humans handle paper.

Because you are losing coverage under your parent’s policy, you qualify for a special enrollment. That means you can apply outside of the annual open enrollment period. Your coverage will usually end during your 26th birthday month but check with the plan to find out exactly when.

You can apply as soon as 60 days before your 26th birthday and wait as long as 60 days after your birthday. But please don’t wait that long because you will be going without coverage between the time your parent’s plan ends and your new plan starts.

Turning 26 Step 6 – Make your first payment

A health insurance company will not issue your policy until you’ve made your first payment, often called a “binder payment”. The best way to make the binder payment is online at the time of your application, although that option is not always available. You can make it later by calling the insurance company or even mailing a check but you will run the risk of missing the payment deadline and voiding your application.

Turning 26 Step 7 – Open your mail

If you get your health insurance through Covered California, don’t ignore your physical mailbox! Covered California loves to send mail and you’ll be tempted to set it aside without opening it. Resist that temptation. You may need to verify your income or your citizenship. If you fail to respond to those letters, you may find your subsidy has disappeared or your health insurance has been cancelled. Either one could spell disaster.

That’s it!

Now that you have the best health insurance you can afford with access to the doctors you need most, you’ll want to keep your plan going. Pay your bill and ask your agent any questions that arise.

Remember, they work for you.

Need help?

Castaline Insurance Agency can help with qualifying for a subsidy, checking doctors, figuring out coverage, or applying for health insurance.

Please feel free to get in contact with us. We’re here to help.